Term loans serve as a vital financial tool for individuals and businesses alike, providing access to capital for various purposes such as business expansion, asset acquisition, debt consolidation, and personal financing. In India, obtaining a term loan involves navigating through a series of steps and considerations to ensure a smooth and successful borrowing experience. Here’s a comprehensive guide on how to secure a term loan in India:

10 Steps to Get a Term Loan in India

1. Understanding Term Loans

Before diving into the loan application process, it’s essential to understand what is a term loan. These loans are a type of borrowing where a lender provides a lump sum amount to a borrower, which is repaid over a predetermined period, usually with fixed or variable interest rates. Term loans may be secured or unsecured, depending on the borrower’s creditworthiness and the collateral offered.

Read: How to Get a Working Capital Loan in India

2. Assessing Financial Needs

The first step in obtaining a term loan is to assess your financial needs and determine the purpose for which you require funding. Whether it’s funding a business venture, purchasing equipment, renovating a property, or financing higher education, clarity on your financial requirements will help you identify the most suitable loan options and lenders.

3. Researching Lenders and Loan Products

Once you’ve identified your financial needs, the next step is to research potential lenders and loan products available in the market. Banks, non-banking financial companies (NBFCs), and online lending platforms offer a variety of term loan options tailored to different borrower profiles and requirements. Compare interest rates, loan terms, eligibility criteria, and repayment options to find the best fit for your needs.

Read: Best Business Loans in India

4. Evaluating Eligibility Criteria

Before applying for a term loan1, it is essential to assess your eligibility based on the lender’s criteria. Lenders typically consider factors such as credit score, income stability, employment status, age, existing debt obligations, and collateral (if applicable) when evaluating loan applications. You must review the eligibility requirements of various lenders to determine your chances of approval.

5. Preparing Documentation

Gathering the necessary documentation is a crucial step in the loan application process. Common documents required for a term loan application in India may include:

- Proof of identity (Aadhar card, PAN card, Passport)

- Proof of address (utility bills, rental agreement)

- Income proof (salary slips, income tax returns, bank statements)

- Business financials (for business loans)

- Collateral documents (property documents, vehicle registration, etc., for secured loans)

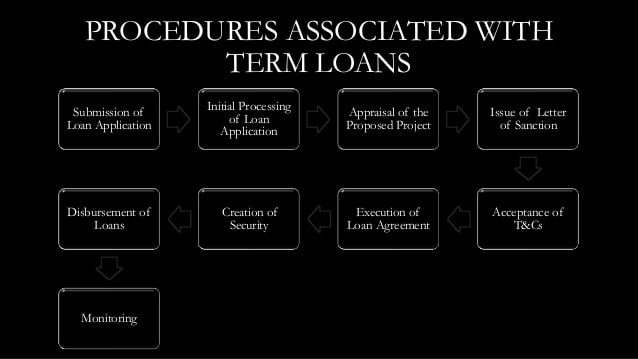

6. Submitting Loan Application

Once you have compiled all the required documents, submit your loan application to the chosen lender through their preferred channel, whether it’s online, in-person at a branch, or through a loan aggregator platform. You will have to provide accurate information and complete all sections of the application form to expedite the processing of your loan request.

7. Undergoing Credit Appraisal and Approval

After receiving your loan application, the lender will conduct a credit appraisal to assess your creditworthiness and repayment capacity. This may involve verifying your credit score, reviewing your financial documents, and assessing the risk associated with lending to you. If satisfied with the appraisal, the lender will approve your loan application and provide you with a loan offer.

Read: How to Apply for a Loan Against Property

8. Negotiating Terms and Conditions

Review the loan offer carefully, paying attention to the terms and conditions, interest rates, fees, and repayment schedule. If necessary, negotiate with the lender to secure favourable terms that align with your financial goals and preferences. Seek clarification on any unclear terms before accepting the loan offer.

9. Disbursement of Funds

Upon acceptance of the loan offer and completion of any formalities, the lender will disburse the loan amount to your designated bank account. Ensure that you use the funds prudently for the intended purpose and adhere to the agreed-upon repayment schedule to avoid defaulting on the loan.

Read: How to Get a Business Loan in India

10. Repayment of the Loan

Make timely repayments of the loan as per the agreed-upon schedule to maintain a positive credit history and avoid penalties or adverse consequences. Set up automated payments or reminders to ensure that you don’t miss any installments. Consider making prepayments or lump sum payments if you have surplus funds to reduce the overall interest cost and shorten the loan tenure.

In conclusion, securing a term loan in India requires careful planning, research, and preparation to navigate the loan application process effectively. By understanding your financial needs, evaluating loan options, meeting eligibility criteria, and adhering to repayment commitments, you can access the capital you need to achieve your goals and aspirations.

Frequently Asked Questions

What is a term loan, and how does it differ from other types of loans?

A term loan is a type of borrowing where a lender provides a lump sum amount to a borrower, which is repaid over a predetermined period with fixed or variable interest rates. Unlike revolving credit facilities such as credit cards or lines of credit, term loans have a specified loan term and fixed repayment schedule.

What are the eligibility criteria for obtaining a term loan in India?

Eligibility criteria for term loans in India vary depending on the lender and the type of loan. Common eligibility requirements include a minimum age of 21 years, stable income or business revenue, satisfactory credit history, and the ability to provide collateral or guarantors (if required).

What are the factors that determine the eligibility for a term loan?

Banks and financial institutions take into account several factors before sanctioning term loans to fund seekers. Some of the aspects are mentioned below:

- Promoters background

- Business model

- Operational performance

- infrastructure

- Cost

- Location

- Collateral security

- Present financial performance

- Projected financial performance

- Credit repayment track record

- External credit rating

The credit decision is taken on a composite of the above factors.

How does my credit score impact my chances of getting a term loan?

Your credit score plays a significant role in determining your eligibility for a term loan and the interest rate offered by lenders. A higher credit score indicates a lower credit risk and may qualify you for better loan terms, while a lower credit score may result in higher interest rates or rejection of the loan application.

What documents are required to apply for a term loan in India?

Common documents required for a term loan application in India include proof of identity (Aadhar card, PAN card), proof of address (utility bills, rental agreement), income proof (salary slips, income tax returns), business financials (for business loans), and collateral documents (property documents, vehicle registration).

What factors should I consider when choosing a lender for a term loan?

When selecting a lender for a term loan, you need to consider factors such as interest rates, loan terms, fees, reputation, customer service, and flexibility in repayment options. Compare offerings from multiple lenders to find the best fit for your financial needs and preferences.

How long does it take to get approval for a term loan in India?

The time taken to get approval for a term loan in India varies. It depends on factors such as the lender’s processing time, completeness of documentation, credit appraisal process, and loan amount. In general, it may take anywhere from a few days to a few weeks to receive approval for a term loan.

Can I prepay or foreclose a term loan before the end of the loan term?

Yes, most lenders allow borrowers to prepay or foreclose a term loan before the end of the loan term. However, prepayment penalties or charges may apply, depending on the terms and conditions of the loan agreement. It’s advisable to check with the lender regarding prepayment options and associated costs before making any early repayments.

What should I do if my term loan application is rejected?

If your term loan application is rejected, try to understand the reasons for rejection and address any deficiencies or issues identified by the lender. You may consider improving your credit score, reducing existing debt obligations, providing additional documentation, or exploring alternative lending options to increase your chances of approval in the future.

Rupak Chakrabarty is the Editor at NextWhatBusiness and a business strategy analyst with over two decades of hands-on experience advising small and mid-sized businesses. His work focuses on entrepreneurship, franchise models, MSME funding, and business planning, with an emphasis on practical decision-making over theory. When not writing or consulting, he enjoys adventure sports, speed, and exploring stories behind businesses.